Pakistan’s LNG surplus crisis: Assessing evolving energy dynamics and the need for flexibility

Download Briefing Note

Key Findings

Global energy markets face rising uncertainty amid shipping disruptions resulting from the closure of the Strait of Hormuz due to the current Middle East conflict. Asian economies, dependent on imported liquefied natural gas (LNG), are increasingly exposed to energy security risks.

Pakistan should explore alternative energy sources and reduce reliance on LNG for power generation. Rapid growth in solar generation and lower grid consumption in the country provide a hedge against dependence on global LNG.

An over-reliance on long-term, rigid contracts for energy security in Pakistan had led to a surplus of LNG before the current Middle East crisis. High LNG costs and rising solar power led to a surplus of 177 LNG cargoes from 2026 to 2031, threatening the country’s gas distribution network with potential damage.

Pakistan’s current strategies focus on alleviating short-term supply shortages and price volatility, but without comprehensive reforms, the country may return to an LNG surplus once Middle East tensions ease. The upcoming price review with Qatar Petroleum for 60 cargoes under a 2016 agreement should seek reduced volumes and greater flexibility.

The United States (US)-Israel war with Iran has severely disrupted global energy markets, with oil and gas prices rising sharply in response. Iran’s effective closure of the Strait of Hormuz — through which approximately 20% of global liquefied natural gas (LNG) supply passes — has placed South Asian economies, including Pakistan, Bangladesh, and India, at significant risk of supply shortages.

According to data from Kpler, Qatar and the United Arab Emirates together supply 99% of Pakistan's LNG imports, 72% of Bangladesh's, and 53% of India's. In these countries, LNG consumption is concentrated in power generation and industrial sectors. In response to supply constraints, India has rationed supply to its industrial sector, Bangladesh has turned to the spot market, and Pakistan has implemented an emergency gas management plan.

Under Pakistan’s plan, domestic and residential supply remains a priority, while around 78 million cubic feet per day (mmcfd) of LNG supply to the fertilizer sector has been suspended. The regasification rate at two LNG terminals has been reduced to 100 mmcfd from 500 mmcfd, as supplies from two vessels received before the conflict are being processed to extend coverage until the end of March. Additionally, 350 mmcfd of domestic gas, previously curtailed to maintain line pack pressures, has been brought back online to ease supply pressures.

Although emergency measures are designed to deal with potential disruptions from the Iran conflict, Pakistan actually had an LNG surplus as recently as January 2026, with average LNG plant utilization below minimum dispatch levels. As a result, the government was diverting excess cargoes to other markets. Consequently, the country may withstand any temporary LNG shortages if the Middle East crisis is contained in a few weeks. The record levels of distributed solar additions and declining grid consumption may also provide a buffer against any demand destruction in the power sector, which accounts for a significant portion of imported LNG purchases.

Without substantial changes to existing demand consumption (which may shrink further during the current conflict), Pakistan may return to a surplus LNG situation unless timely reforms are enacted.

How did Pakistan’s LNG surplus emerge?

Pakistan was once considered to be a major growth market for LNG demand in Asia. However, LNG consumption has significantly declined recently, driven by structural shifts caused by weakening gas demand, a rapid rise in distributed renewable energy, and uncompetitive prices resulting from rigid contractual obligations.

As a result, an LNG glut emerged at the end of 2024, initially forcing the deferment of five LNG import cargoes from 2025 to 2026. The surplus continued to worsen in 2025. A lack of on-ground storage in Pakistan, combined with fixed off-take obligations to purchase LNG from Qatar, resulted in excess LNG in the energy system and threatened the country’s physical gas transmission infrastructure. As LNG-to-power demand did not materialize, Pakistan ultimately had to renegotiate its long-term supply agreements with Qatar and Italian gas producer ENI for the reselling of 45 excess cargoes to regional markets on a Net Proceeds Differential (NPD) basis between 2026 and 2027.

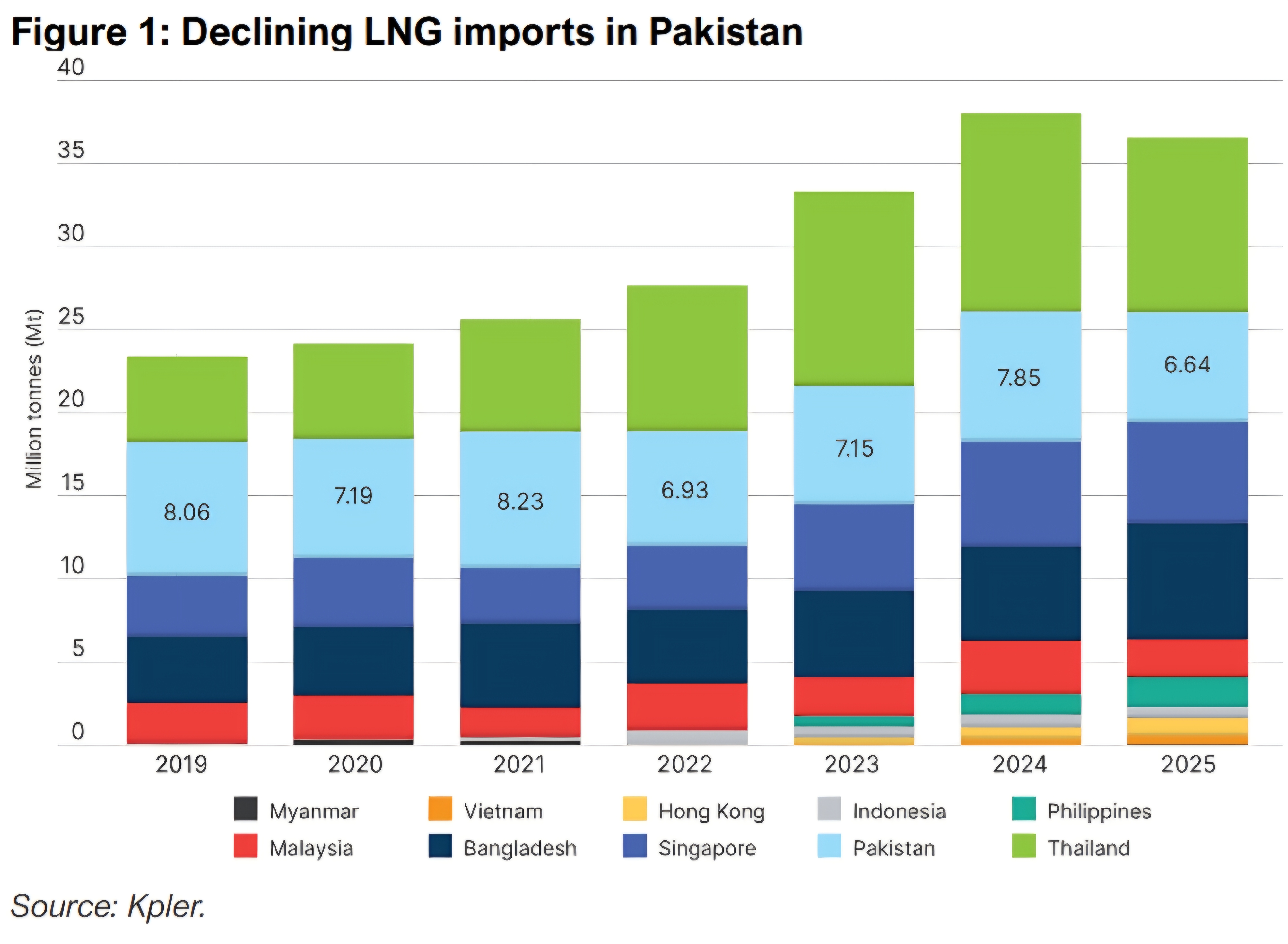

LNG imports to Pakistan fell following the Russia-Ukraine crisis in 2022, before rebounding in fiscal year (FY) 2024, reaching 7.85 million tonnes (Mt) — a 13% increase compared to 2023 and the first growth recorded since 2021 (Figure 1). While consumption by the power sector and the fertilizer industry rose, it was short-lived as cost impacts and weak demand set in, leading to a system surplus for the first time in the last quarter (Q4) of 2024.

Pakistan’s power sector is a major consumer of LNG, accounting for approximately 70% of total LNG imports. However, persistently high LNG prices have rendered LNG-based energy generation uncompetitive, pushing such plants down the economic merit order.

Pakistan experienced a 1.21 Mt decline in LNG consumption in 2025. According to research by the Institute for Energy Economics and Financial Analysis (IEEFA), this has resulted from a reduction of 4.5 terawatt-hours (TWh) of power generation from LNG plants in the power sector (including energy utility K-Electric), while the rest can be attributed to a drop in the industrial sector’s offtake.

For instance, in September 2025, the power sector reportedly consumed only 510 mmcfd of LNG, compared with an allocated capacity of 800 mmcfd. Meanwhile, exporting industries also reduced their consumption from 350 mmcfd to just 100 mmcfd, attributing this shift to rising LNG prices.

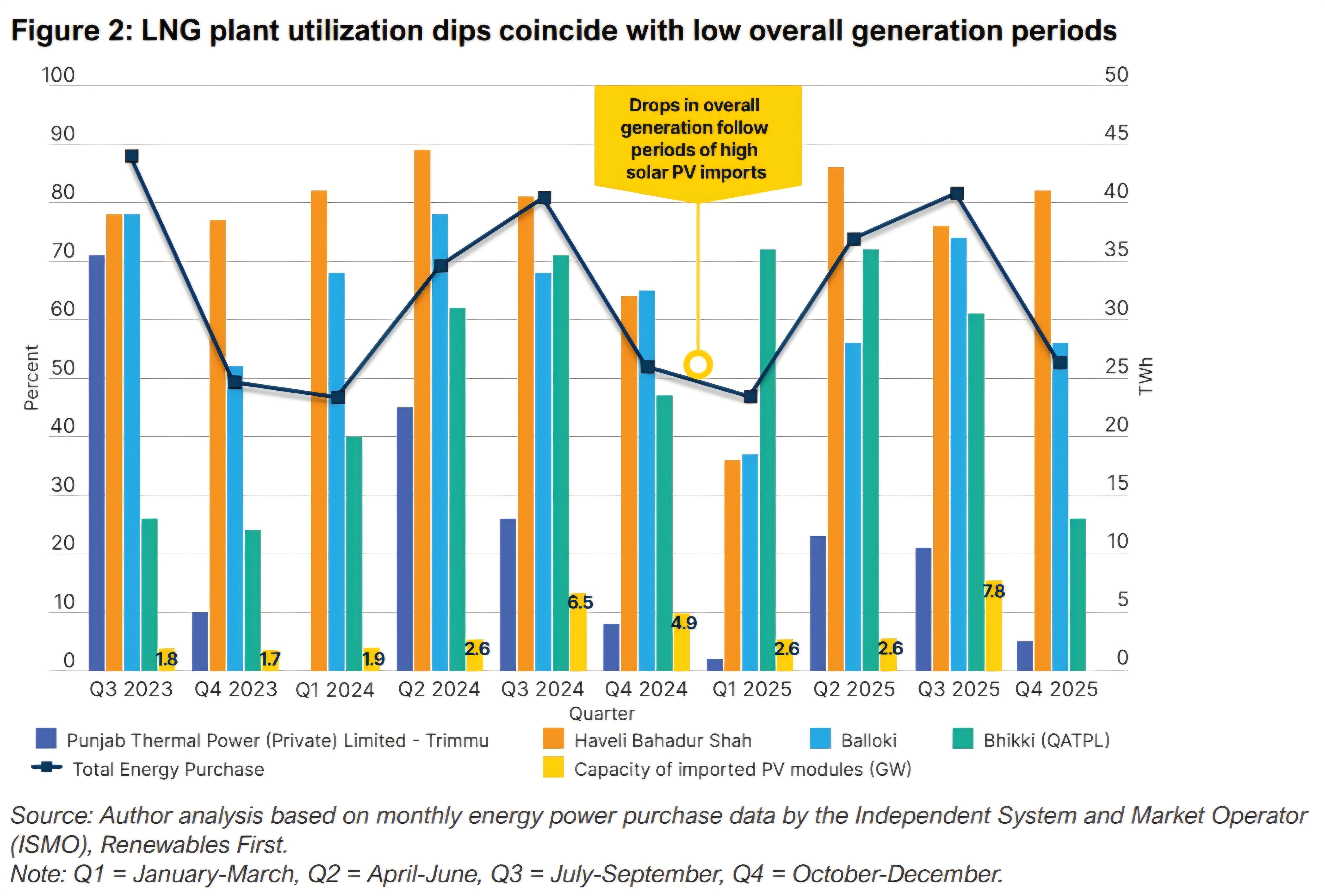

A majority of the power sector’s LNG volume is supplied to four 1,200-megawatt (MW) state-owned LNG plants — Bhikki, Balloki, Haveli Bahadur Shah, and Trimmu. Originally designated as must-run projects with a 66% minimum LNG take-or-pay arrangement (revised to 50% in 2025), these plants are subject to forced dispatch to avoid penalties or prevent line pack pressure buildup.

According to the National Electric Power Regulatory Authority (NEPRA) performance evaluation report 2025, utilization rates for Bhikki, Balloki, and Haveli Bahadur Shah plants were 61.6%, 53.5%, and 63%, respectively, in FY2025, while Trimmu only averaged 16% across the entire year. Figure 2 shows how utilization fluctuated through the year, coinciding with periods of high solar photovoltaic (PV) imports and low grid-based consumption. Plant utilization at Trimmu plummeted during the first quarter (Q1) of 2025, with a three-month average utilization of just 2%.

While government-owned plants are required to operate at specific levels, the plant at Trimmu reflects market realities. Despite an oversupply of LNG in the country, the plant has been unable to price into the system during periods of high solar output and low demand.

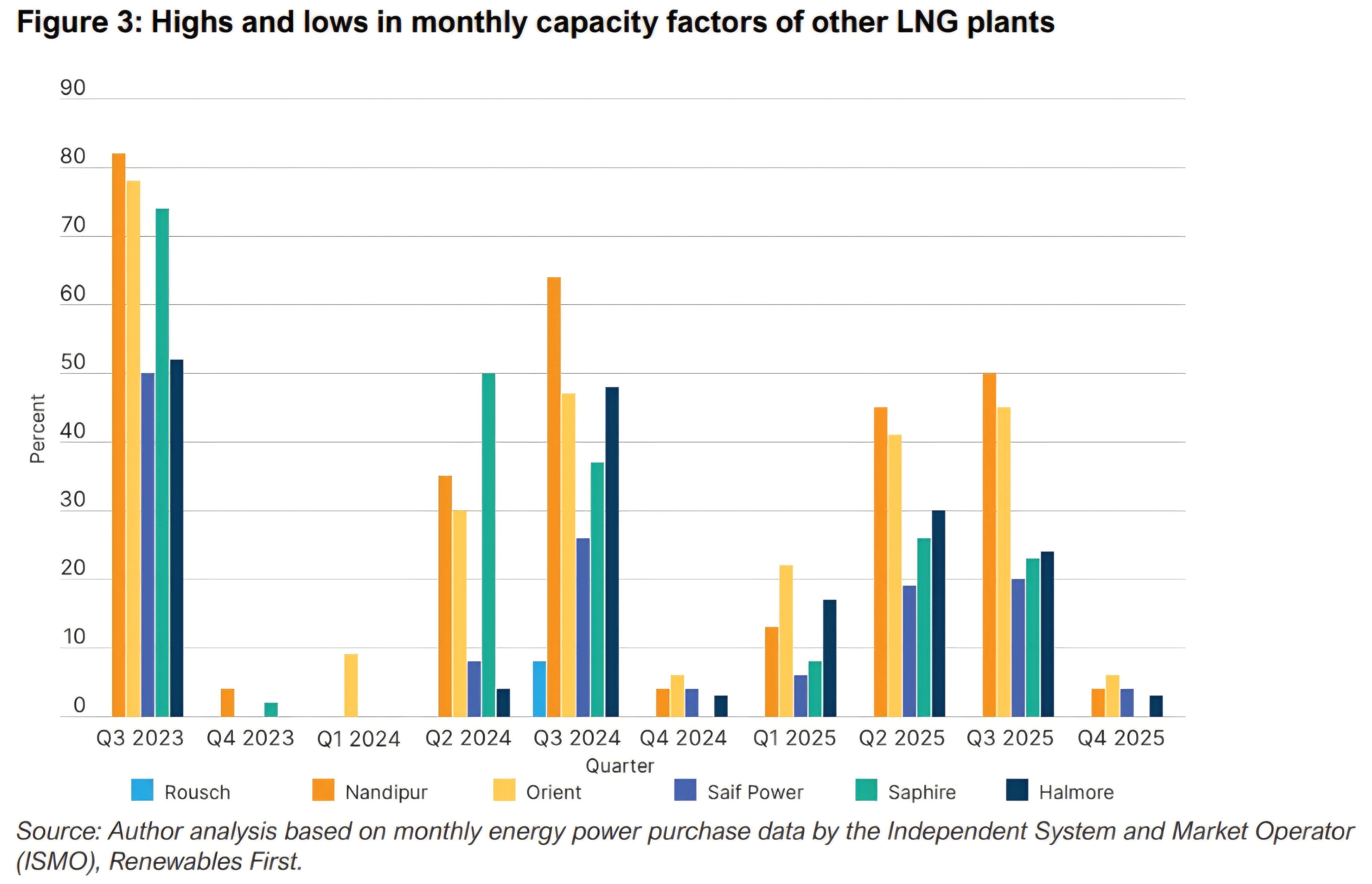

A similar situation prevails for the other six small-to-medium-sized (200–400MW) thermal plants operating on LNG. Utilization rates began declining after Q4 2024, with averages below 50% for most LNG plants throughout 2025, dropping as low as 0–4% for Nandipur, Saif Power, Sapphire, and Halmore power plants (Figure 3).

Rapid solarization provides a hedge against LNG dependence

Record distributed solar additions since 2023 have also impacted centralized power generation. Pakistan’s installed distributed solar capacity reached 34 gigawatts (GW) in 2025, with an estimated 25GW connected to the grid through net-metered and non-net-metered residential, commercial, and industrial installations. Grid-based demand fell nearly 11% in FY2025 compared to FY2022 levels, reducing offtake from expensive power generation technologies, including imported coal, High-Speed Diesel (HSD), Heavy Furnace Oil (HFO), and LNG. With solarization trends expected to continue and overall Gross Domestic Product (GDP) growth remaining subdued, Pakistan’s electricity demand outlook for 2026 is conservative. Consequently, government LNG buyers are seeking to offload approximately 45 excess cargoes, representing 364 mmcfd. 24 Qatar-contracted and 11 ENI-contracted cargoes are already being diverted to other markets on an NPD basis. An additional surplus of 10 cargoes may materialize if the power sector cannot utilize them.

Curtailment of domestic supply and LNG diversion

The power sector’s inability to absorb excess cargoes often results in a diversion of LNG volumes to the domestic sector. This is an inadequate solution, due to a price mismatch between low retail gas tariffs (based on subsidized domestic gas) and the high cost of imported LNG.

The government routinely diverts LNG to the domestic sector during winter months, when demand is high, adding millions of dollars to the gas sector’s circular debt, which currently stands at PKR3.3 trillion (USD11 billion).

In 2025, lack of storage and the limited capacity of the pipeline distribution infrastructure resulted in line pack pressures above 5 billion cubic feet (Bcf) — the danger threshold for the national gas network. To prevent further escalation of pressure, the government had to curtail production from domestic gas wells with a capacity of 270–400 mmcfd.

State-owned Oil and Gas Development Company (OGDC) posted revenue losses of PKR 43 billion, while international oil and gas exploration companies also reported declining earnings in FY2024–2025. Since LNG is priced at nearly three times the cost of domestic gas, a diversion of LNG supply adds to the gas sector’s circular debt. This is exacerbated by unaccounted for gas (UFG) losses, estimated at around 11.7% of gas handled, arising from theft and technical leakages.

Under such circumstances, contract renegotiation for the diversion of excess LNG cargoes is a pragmatic approach, reducing the gas sector’s exposure to the risk of further non-recovery of diversion costs, curtailment of domestic gas production, and potential damage to gas distribution infrastructure.

The consequences of long-term contracts

Pakistan procures LNG primarily through long-term contracts, after being priced out of the spot market following the Russia-Ukraine crisis. Two 15- and 10-year contracts with Qatar for the supply of 6.75 million tonnes per annum (MTPA) of LNG, or nine cargoes per month, account for the bulk of Pakistan’s LNG consumption. Pakistan also has a 15-year contract with ENI for the supply of 11 Mt (0.75 MTPA), or one cargo per month, and a framework agreement with Azerbaijan's state-owned Socar for an additional cargo per month if needed.

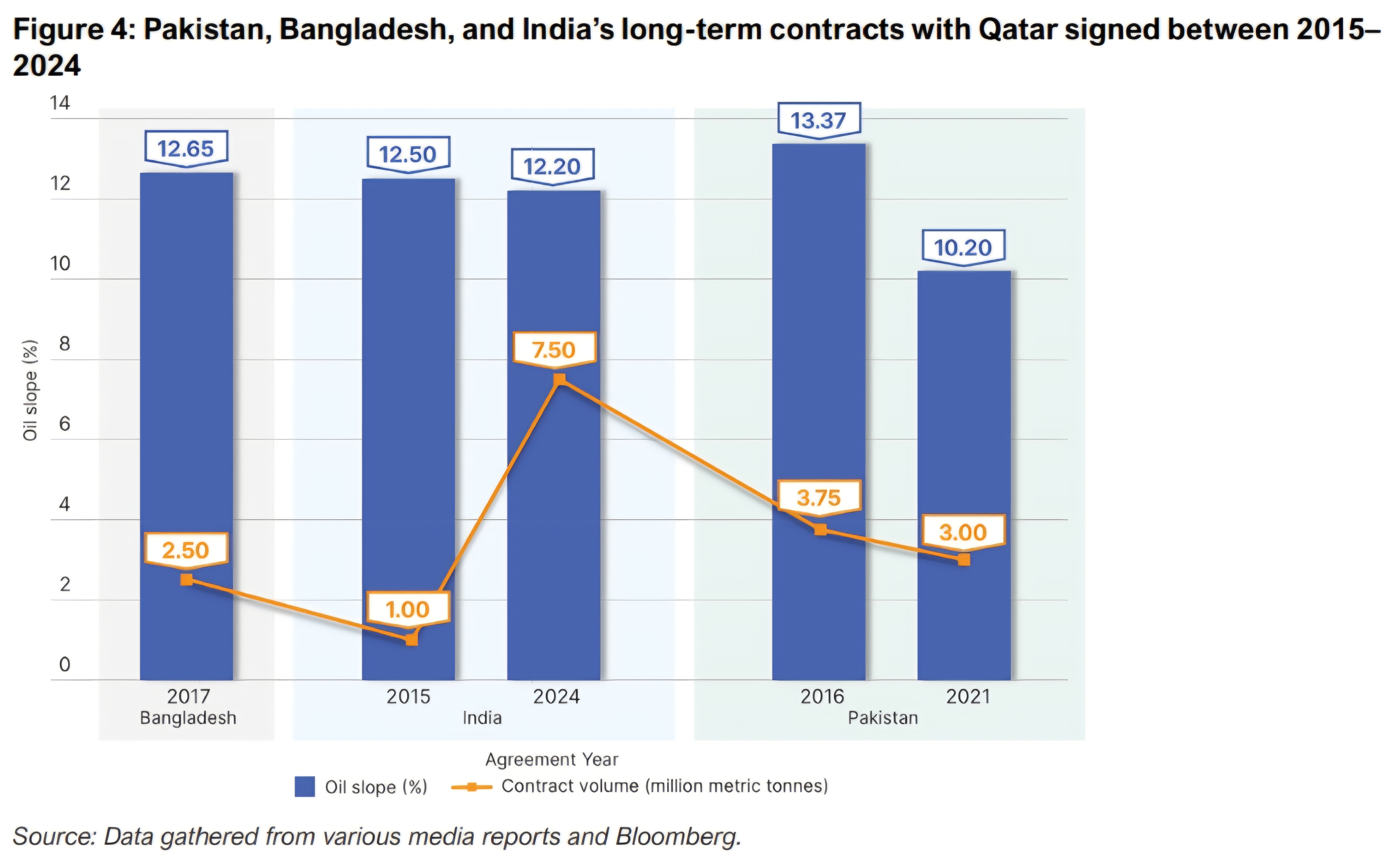

Pakistan’s long-term contracts with Qatar are consistent with regional standards. They are indexed to Brent crude, delivered ex-ship (DES) to a designated port, and without cargo re-routing flexibility. Contract prices reflect a Brent crude slope ranging between 10.2% and 13.37%.

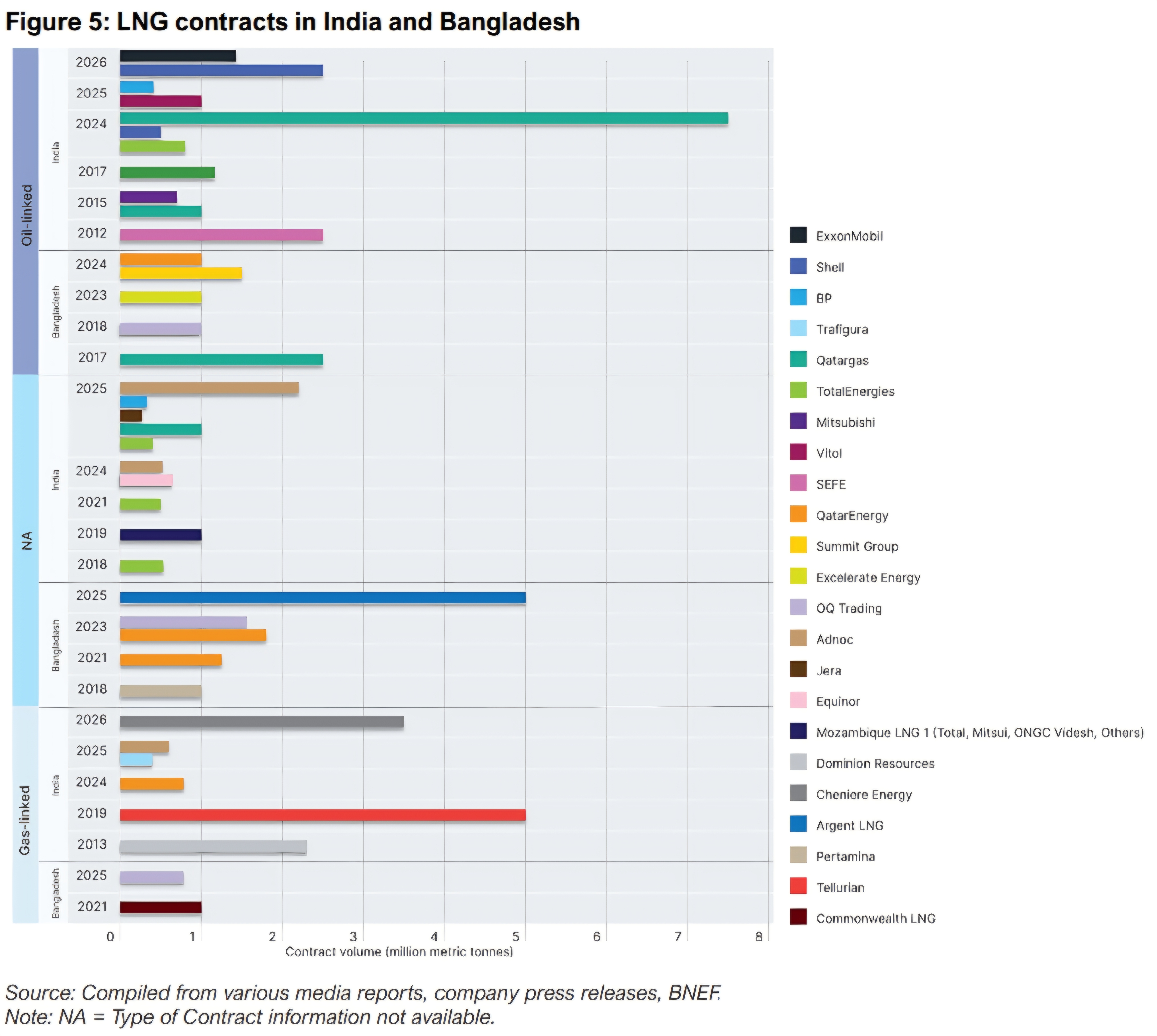

While India and Bangladesh have long-term contracts with Qatar with comparable values, both countries maintain more diversified supply options. These include contracts indexed to Henry Hub pricing, as well as a wide range of short-term agreements with traders and portfolio players, offering more competitive pricing and, in some cases, destination flexibility.

Given prevailing conditions and Pakistan’s subdued future LNG demand outlook, contract renegotiation and the reselling of excess cargoes are practical approaches. However, the challenge extends beyond cargo diversion. Currently, excess cargo diversion has been arranged only until 2026 for contracts with Qatar, and through 2027 with ENI. According to projections by Pakistan’s Petroleum Division, if left unaddressed, there could be an excess of 177 cargoes until 2032, carrying a liability of USD5.6 billion, or higher if oil prices increase.

Impact of contract renegotiation and Pakistan’s upcoming price review

Although Pakistan’s LNG contracts lack destination flexibility, the country can divert cargoes elsewhere through profit/loss-sharing mechanisms or on an NPD basis. For instance, the contract with ENI includes a profit/loss-sharing clause, based on the cargo resale price.

Conversely, under agreements with Qatar, Pakistan has to notify the number of cargoes to be diverted on an NPD basis at the time the annual delivery plan (ADP) is finalized. The cargoes would be resold in the market by Qatar, with any profits during the resale going to Qatar, while any losses incurred would have to be borne by Pakistan.

The 24 diverted Qatari cargoes are likely to be resold to Egypt, once Qatar’s conflict-affected production resumes. In January 2026, Egypt signed a memorandum of understanding (MOU) with Qatar Energy to boost bilateral cooperation in LNG sales and imports, including the supply of up to 24 cargoes during the year.

The agreement had reportedly been signed at a preferential price of USD8–10 per million British thermal units (MMBtu), excluding transportation, regasification, and other associated costs. Pakistan’s Oil and Gas Regulatory Authority (OGRA) issued LNG price notifications for January and February 2026, revealing that the landed price (DES) of LNG in the country is currently USD7.5/MMBtu on average. Since Qatar can sell these cargoes at a profit, Pakistan would not incur any losses in this instance. Depending on how Qatar’s LNG fares in terms of pricing after the Iran conflict is over and the actual price differential, which could be positive, Pakistan may incur a loss. Nonetheless, the financial impact would still be lower than the additional circular debt resulting from LNG diversion to the domestic sector and revenue losses from curtailment of local gas production.

Given Pakistan’s economic instability, reselling cargoes on an NPD basis can be a viable short-term solution. However, the contract terms favor the seller compared to a profit/loss-sharing mechanism. While cargo cancellation or long-term rescheduling may not be an option given stringent take-or-pay obligations, Pakistan’s upcoming price review with Qatar Petroleum in March 2026 — covering 60 cargoes at 13.37% Brent slope under a 2016 agreement — may provide a renegotiation opportunity.

Price reviews are becoming increasingly common in Asia, particularly during periods of extreme price volatility. For example, India successfully conducted three public price reviews in 2015, 2017, and 2018, resulting in significant discounts and pricing changes. Similarly, China has also renegotiated contracts with Indonesia and Qatar to raise oil price caps (in favor of Indonesia) or revisited pricing methodologies.

For Pakistan, the 13.37% slope of its Qatar contract is higher than the average awarded to other South Asian countries (Figure 4). Consequently, there may be room for downward revision. As LNG markets evolve from tight supply conditions during 2021–2022 to more stable supply led by additional production from the US and Qatar, buyers are expected to prioritize flexibility and lower prices.

Currently, Pakistan’s contracts with Qatar do not permit a reassessment of contracted volumes. However, price reviews can include volume flexibility terms, such as modifying buyers’ rights to nominate additional cargoes or Upward Quantity Tolerance (UQT) — which are already a part of Pakistan’s contracts — or reducing cargo volumes or Downward Quality Tolerance (DQT).

Alternatively, hardship clauses could also be invoked to prevent long-term economic impairment, given Pakistan’s financial strain. The key to a sustainable outcome is a carefully negotiated trade-off: volume flexibility in exchange for scheduling flexibility may be an option. However, buyer flexibility comes at a cost, and Pakistan would likely have to pay a premium for flexible contracts alongside the current pricing regime. Another option is to be amenable to seller flexibility, for instance, allowing Qatar to divert cargoes to other markets when it chooses.

While spot markets have posed significant financial risks to Pakistan’s energy system in the past, the global LNG market may be poised for a shift once the current crisis is resolved. An anticipated supply glut may change conditions from a seller’s to a buyer’s market, affording Pakistan greater flexibility to buy cargoes from more liquid spot markets when prices are favorable. Contract renegotiations with Qatar should reflect this change and account for both reduced volumes and greater flexibility.

Revised contract terms could include higher DQTs, destination and timing flexibility (seasonal volume fluctuations embedded in the contracts), or shorter contract terms.

Conclusion: Rising tensions in the Middle East present a reality check

The US-Israel war with Iran has heightened military tensions and resulted in strikes on energy infrastructure across the Gulf region and disruption to traffic through the Strait of Hormuz. Qatar halted production and declared force majeure after its Ras Laffan liquefaction facility was also struck.

As oil and gas wholesale prices surge in response, there are likely to be implications for Pakistan because of its oil-indexed contracts, leading to higher landed prices if the conflict continues. The price review with Qatar is also likely to face delays as its priorities shift to restoring supply chain disruptions, potentially delaying the upcoming supply glut.

While Pakistan is ramping up domestic production and exploring alternate routes for oil deliveries, a shift away from LNG-based power generation would be advantageous in the short term, protecting against rising power generation costs and over-reliance on global LNG markets. Qatar may also be more amenable to granting Pakistan the flexibility to schedule deliveries amid production downturns and delayed timelines.

The LNG surplus in Pakistan and its ensuing economic impact is more than a contractual dilemma. The rigid, long-term take-or-pay contracts, once valued for energy security, have become a financial burden in a market that prioritizes flexibility and low-cost generation.

Renegotiating contracts to offload excess LNG cargoes may provide immediate, if costly, relief, but does not address the root cause — an energy procurement strategy misaligned with the country's evolving demand and the accelerating development of renewable energy. Rapid growth in solar power generation and lower grid-based consumption provide a hedge against reliance on global LNG markets to meet power demand, especially as tensions rise in the Middle East.

Pakistan should continue to boost solar development, while embracing new opportunities. This may include reducing contracted LNG volumes below total demand, understanding that LNG demand does not have to be fully covered by long-term contracts. The country should pivot from reactive crisis management to a proactive strategy built on agile procurement, sophisticated forecasting that embraces distributed generation, and enhanced institutional capacity to secure flexible terms.