Fostering Bangladesh’s energy transition

Download Full Report

View Press Release

Key Findings

Heightened risks of global supply disruptions, fiscal burden, and rising costs underscore the importance of fostering Bangladesh’s energy transition. Renewable energy, a natural hedge against fossil fuel supply disruptions and price spikes, contributes to 2.3% of the country’s power generation against the global average of around 33.8%. This highlights the need to swiftly shore up the country’s clean energy capacity.

Currency depreciation and the high prices of imported fossil fuels do not fully explain Bangladesh’s soaring power generation cost. Costly peaking plants alongside capacity payments due to high reserve margin and fuel supply shortage make its power significantly expensive, leading to continued fiscal burden.

In FY2024-25, private oil- and coal-fired power plants received capacity payments of BDT9.5/kWh and BDT5.9/kWh respectively, raising the average generation cost substantially. Bangladesh’s reliance on expensive oil-fired plants for 10.7% of power generation is much higher than India (0.02%), Pakistan (0.6%), and Vietnam (0.06%), which creates an immediate opportunity to utilise renewables and contain costs.

Bangladesh could pay a large subsidy of around USD1.07 billion to import LNG to meet its power demand in April-June 2026. Besides accelerating domestic renewable energy, the country may consider tapping into the potential of regional hydropower post 2030 to limit its reliance on LNG.

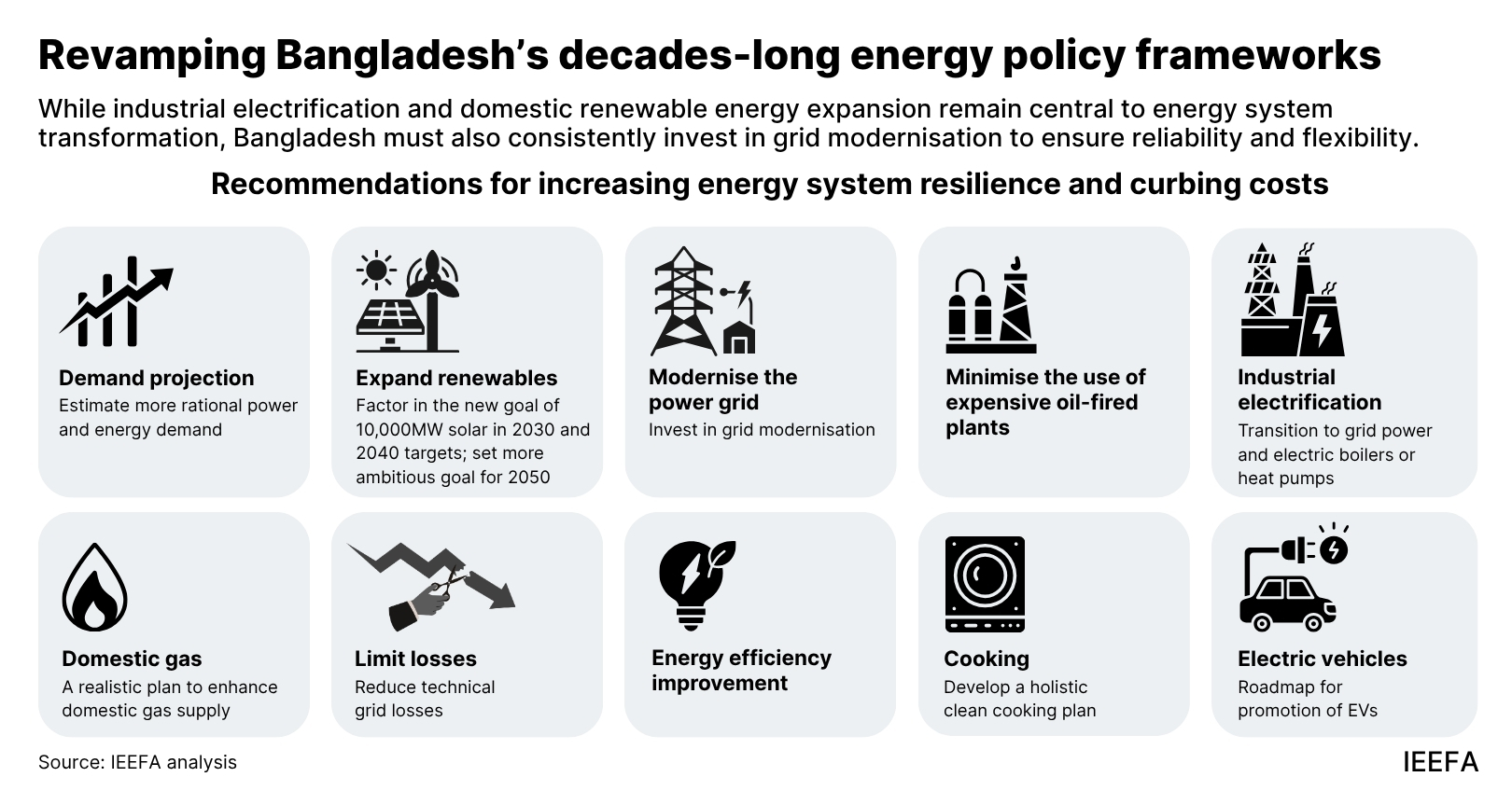

The country could further cut its exposure to volatile fossil fuel markets by containing system loss, enhancing energy efficiency, and maintaining domestic gas supply. For the power sector’s sustainability, Bangladesh should reduce its reserve margin, thereby minimising its high subsidies.

Between fiscal year (FY) 2020-21 and 2024-25, Bangladesh’s primary energy imports surged from 47.7% to 62.5%, intensifying exposure to highly volatile international fossil fuel markets. Limited investment has led to falling domestic gas supplies, raising the country’s dependence on liquefied natural gas (LNG) and other imported fossil fuels. Renewable energy, which provides a natural hedge against fossil fuel price spikes, contributes to only 2.3% of the country’s grid-based power generation. The global average for the same stands at 33.8%. As such, any disruption in the global fossil fuel market immediately affects price-sensitive Bangladesh’s energy system, increasing its fiscal burden.

Between FY2020-21 and FY2022-23, average power generation costs soared from BDT6.61/kilowatt-hour (kWh) (USD0.054/kWh) to BDT11.33/kWh (USD0.092). While high prices of imported fossil fuels, especially following the Russia-Ukraine war, and the United States Dollar’s (USD) appreciation against the BDT are generally considered responsible for the spike in costs, this study shows that capacity payments and expensive peaking plants have also contributed significantly.

For instance, Bangladesh’s power sector registered a large reserve margin of 61.3% (58.6% based on derated capacity) in FY2024-25 due to an insufficient growth in demand, resulting in large capacity payment obligations. IEEFA’s assessment concludes that private coal-fired and furnace oil-based plants received an average capacity payment of around BDT5.9/ kilowatt-hour (kWh) (USD0.048/kWh) and BDT9.5/kWh (USD0.077/kWh), respectively. Moreover, insufficient fuel supply increased capacity payment in gas-fired plants. Available data shows that load factor influences average generation costs – plants operating at over 75% load factor and less than 25% load factor generated power at around BDT6/kWh (USD0.049/kWh) and BDT16.85/kWh (USD0.137/kWh), respectively.

Bangladesh’s reliance on oil-fired peaking power plants stood at 10.7% in FY2024-25, as opposed to well below 1% in India, Pakistan, and Vietnam, raising its power generation costs. Besides, high system losses in the gas sector take a toll on the energy and power sectors.

The latest energy supply disruption, from geopolitical tensions in the Middle East, has also affected the country severely. Bangladesh could end up paying around USD1.07 billion in subsidies for LNG imports during April-June 2026, to secure the equivalent amount of LNG imported in the same quarter of 2025, based on the spot price of about USD20/million British thermal units (MMBtu). The foreign currency constraints could ultimately limit the country’s capability to import the required volume of LNG, forcing load shedding. Expensive oil and coal could also increase the subsidy burden. To keep the economy afloat with a sufficient energy supply, Bangladesh has already sought support of about USD2 billion from multilateral agencies.

These challenges highlight the need to revamp Bangladesh’s decades-long energy policy frameworks that are built around imported fossil fuels and inherent inefficiencies. The solutions to the persistent problems lie closer home, such as in expanding domestic renewable energy at scale while limiting fossil fuel-based plants to contain overcapacity.

Further, by tapping into the regional, cost-competitive hydropower potential, Bangladesh could reduce its gas demand, thereby limiting its exposure to price-volatile LNG. For instance, post 2030, a combined hydropower capacity of 6,000 megawatts (MW) for the high-demand March-September period will likely help the country reduce annual gas consumption by up to 257 billion cubic feet (Bcf).

Bangladesh could further assess the opportunity to export power to Bhutan and Nepal during the winter season through the Bangladesh-Bhutan-India-Nepal (BBIN) framework. It could also explore the option of purchasing the highly cost-competitive renewable energy offered in the Indian day-ahead market, thereby reducing its average power generation cost.

The country should encourage industries to shift to grid power, reducing reliance on both captive power and gas boilers, subject to a reliable electricity supply. In addition, demand-side efficiency improvement and reduction in gas sector system losses will likely limit Bangladesh’s growing LNG demand. This will help the country devise a realistic plan for domestic gas capacity addition.

To attract capital for a clean energy transition, the government should enhance investors’ confidence. The recently approved guidelines for utilising public land in renewable energy projects under the Public-Private-Partnership (PPP) model will likely address the challenges in land acquisition in some projects. The government should fix a timeline from land allocation to selection of private partners, tariff negotiation, and project implementation to avoid delays. Moreover, the government should offer a feasible open access tariff for utility-scale renewable energy projects under the Corporate Power Purchase Agreement (CPPA) to provide the opportunity to industries like garments and corporates to green their operations as part of their greenhouse gas mitigation targets. Besides, distributed renewable energy systems require an urgent waiver/reduction in high import duties for their rapid scale up.

While industrial electrification and domestic renewable energy expansion are central to energy system transformation, Bangladesh should also consistently invest in grid modernisation for reliability and flexibility.

The global energy supply disruption, triggered by the geopolitical crisis in the Middle East, again shows that imported fossil fuels make Bangladesh’s energy system vulnerable and increase its fiscal burden. The country should now design an ecosystem that fosters an effective energy transition, gradually insulating it from the high price volatility of fossil fuels in the international market.

Related Content