Cambodia's rooftop solar barriers persist amid utility-scale solar surge

Download Briefing Note

Key Findings

Steadily expanding utility-scale solar is transforming Cambodia’s electricity system ahead of schedule. At almost 1.5 gigawatts (GW), solar capacity already exceeds the 2030 and 2035 targets under the Power Development Master Plan (PDP) and supplies 10% of the country’s electricity mix.

Rooftop solar deployment in Cambodia remains constrained by government concerns over grid stability and impacts on the state-owned utility. Export-oriented manufacturers cite low-cost rooftop solar access as a necessity for competitiveness, yet policy barriers continue to limit adoption.

Cambodia’s compensation tariff for rooftop solar adopters exceeds grid impact costs by three to four times, undermining the financial case for rooftop installations and extending the payback period for medium and large systems by nearly two years.

Cambodia has some of the highest electricity tariffs in Asia, and the planned commissioning of a liquefied natural gas (LNG)-to-power plant could further raise prices. Removing rooftop solar barriers would unlock Cambodia’s solar potential and provide the country with access to low-cost, decarbonized electricity.

Introduction

Utility-scale solar expansion is transforming Cambodia’s electricity system ahead of schedule, aligning with the government’s view that solar is integral to meeting rapidly growing electricity demand and achieving national climate goals.

Despite strong growth in utility-scale solar projects, concerns over grid reliability and the cost impacts of rooftop solar for grid-reliant consumers have translated into policy barriers that constrain broader solar development, even as solar remains among the lowest-cost sources of electricity generation in Cambodia.

Recent advocacy by garment exporters and manufacturers has been successful in removing a prohibitively expensive capacity payment system for rooftop solar installations. However, a replacement scheme — framed as a compensation tariff — remains a barrier to the adoption of renewable energy for commercial and industrial businesses. Moreover, the annual rooftop solar quota of 30 megawatts (MW) sets a low ceiling for deployment.

These restrictive rooftop solar policies remain at odds with the needs of Cambodia’s export-oriented manufacturers. Rooftop solar can lower production costs, improve industrial competitiveness, and attract investment from corporations with supply chain decarbonization targets.

As policy barriers impede rooftop solar growth, the commissioning of the country’s first liquefied natural gas (LNG)-to-power project in 2027 could raise electricity tariffs and increase the carbon intensity of the national grid. For many companies operating in Cambodia, accelerating low-cost, rooftop solar deployment would become increasingly necessary. A mechanism allowing the state-owned utility to purchase surplus solar generation from these rooftop installations could also help offset electricity rate pressures as high-cost LNG capacity is integrated into the grid.

An overview of recent solar advances in Cambodia

Several government announcements in the last year reflect the expanding role of solar in Cambodia’s electricity system.

The updated Nationally Determined Contribution (NDC 3.0) cites utility-scale solar expansion as integral to reducing fossil fuel dependency, lowering energy sector emissions, and achieving a 72%–80% renewable energy capacity target by 2035. In October 2025, the Ministry of Mines and Energy (MME) identified solar as central to achieving its target of 70% renewable energy capacity by 2030. Cambodia has further signaled its support for the energy transition by joining the Fossil Fuel Treaty Initiative, an alliance advocating for a global shift away from fossil fuels through accelerated renewable energy deployment.

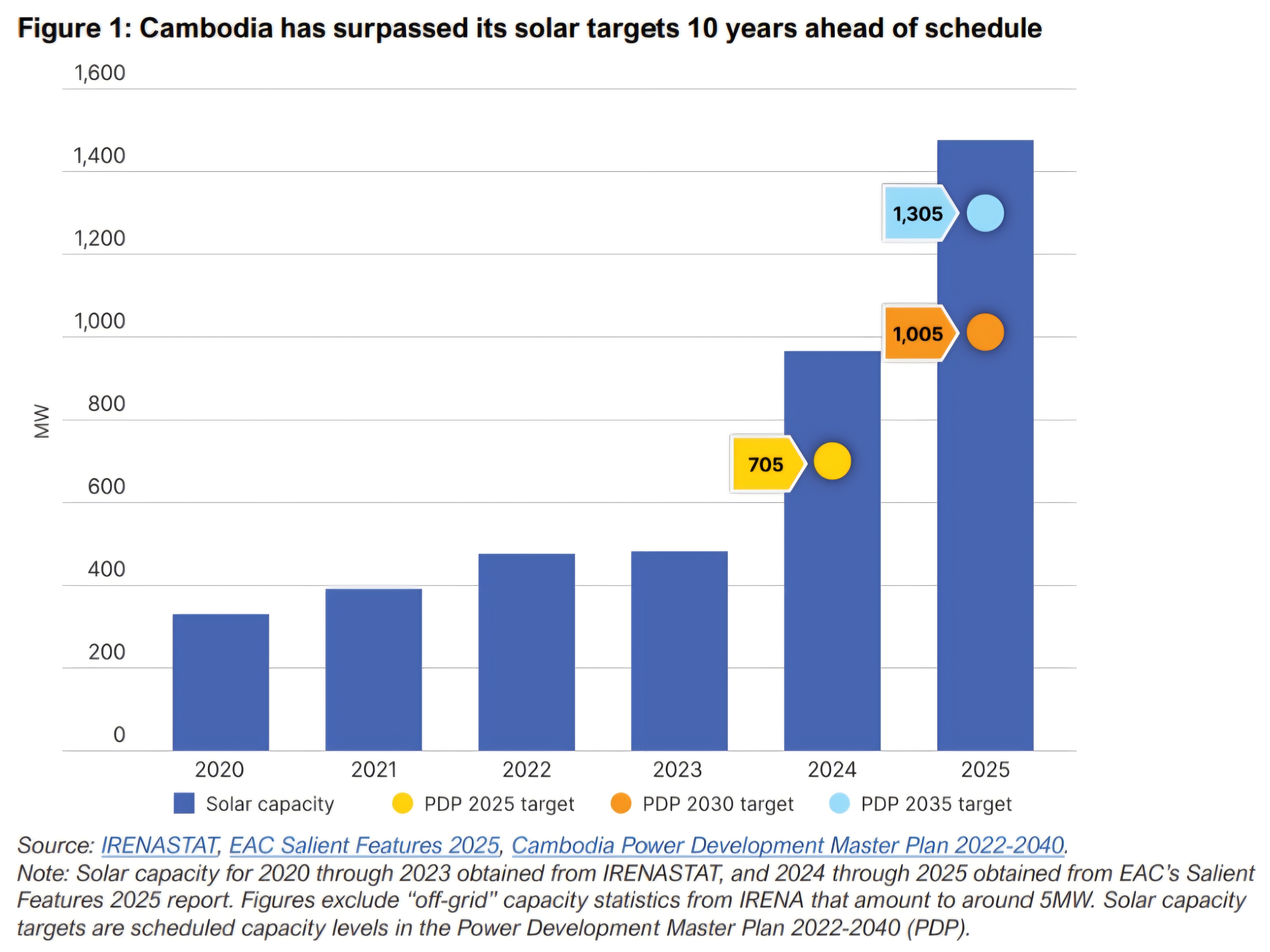

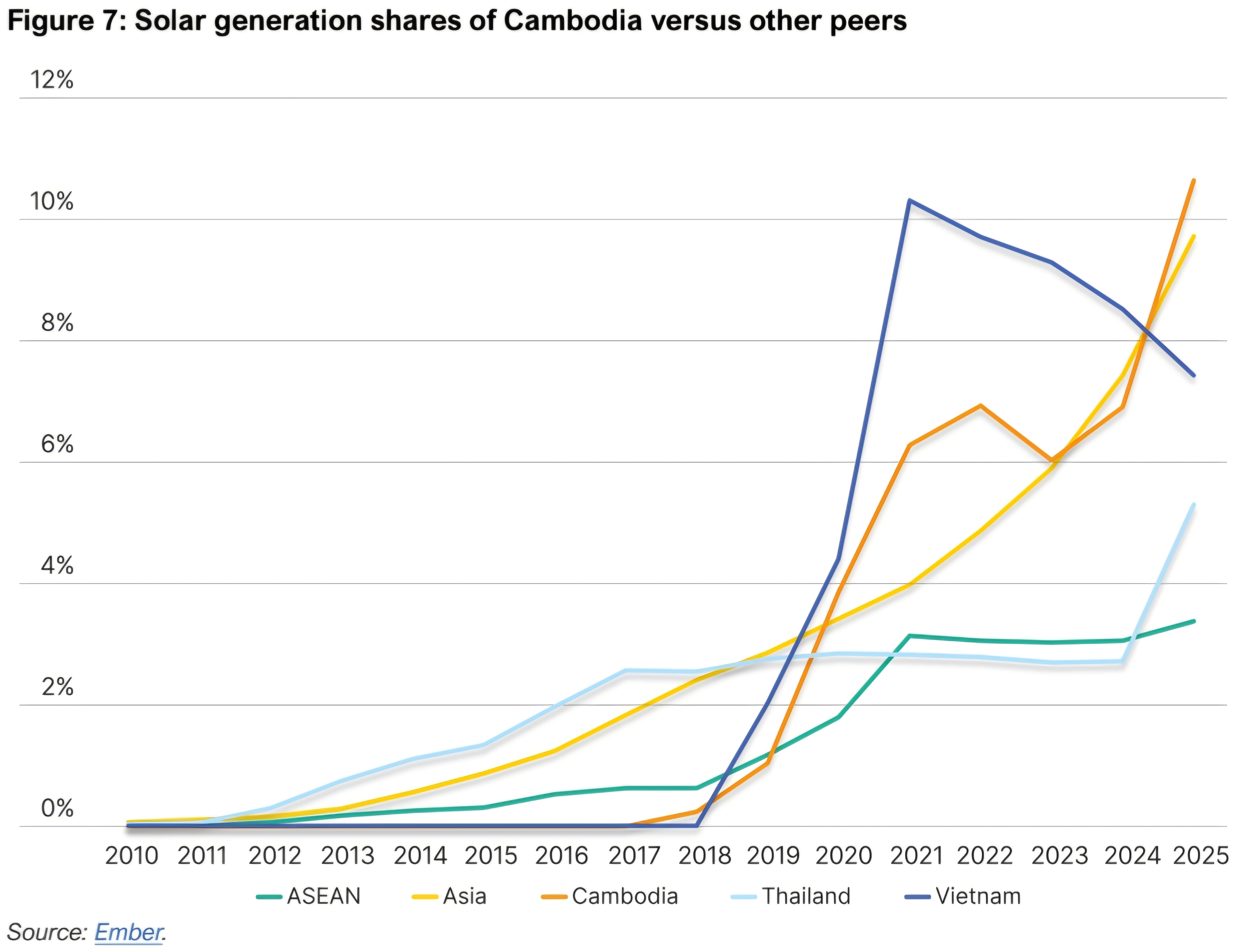

Cambodia’s renewable deployment is already surpassing expectations. The country’s Power Development Master Plan 2022-2040 (PDP), a key framework underpinning NDC 3.0, envisioned solar capacity would reach 705MW in 2025, 1 gigawatt (GW) in 2030, and 1.3GW by 2035. According to the Electricity Authority of Cambodia (EAC), the country surpassed its 2025 PDP target a year early and exceeded its 2030 and 2035 targets well ahead of schedule, reaching almost 1.5GW of installed solar capacity in 2025. Solar now produces over 10% of Cambodia’s electricity generation.

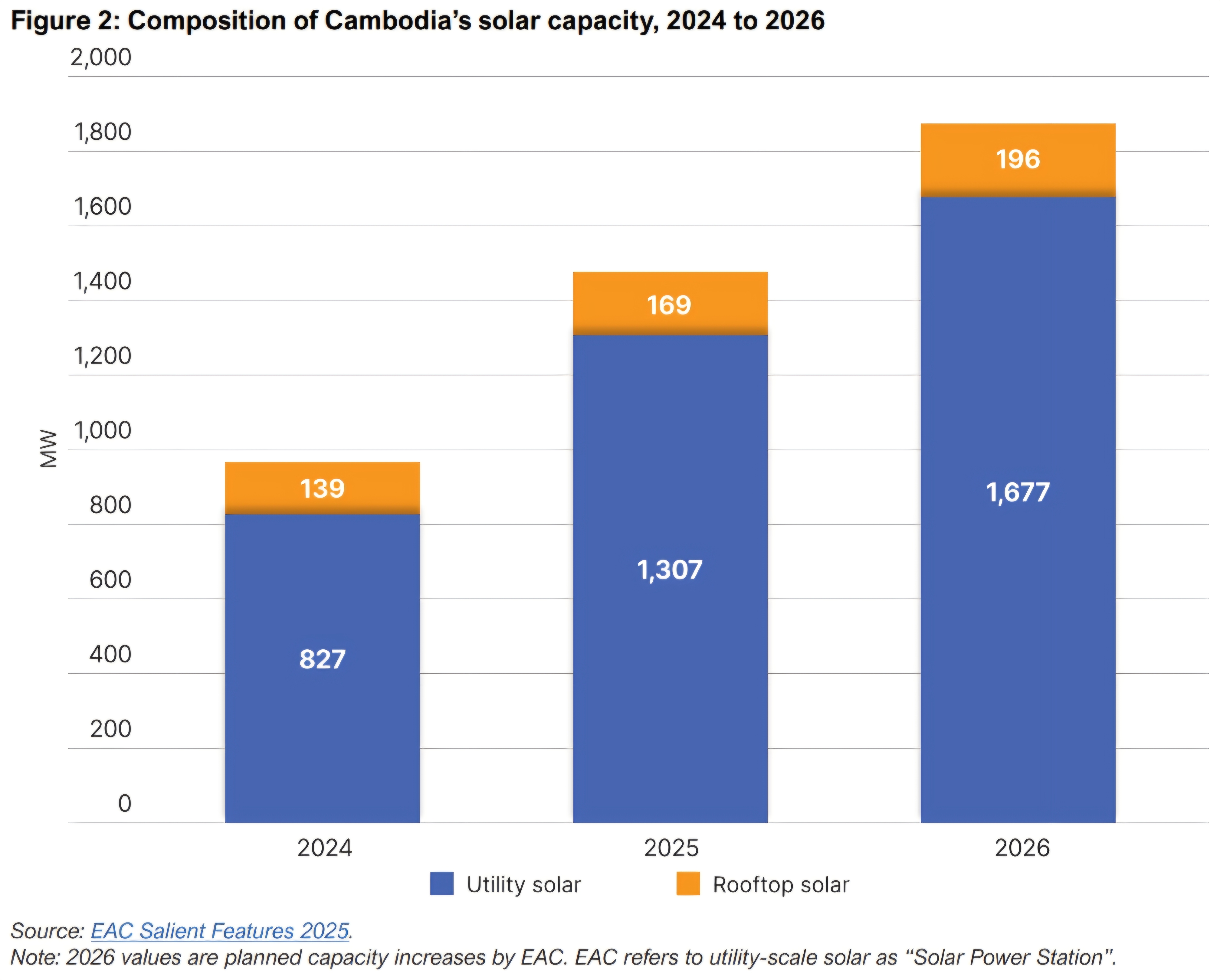

This increase in solar capacity has been driven almost entirely by utility-scale projects. Since the EAC began reporting rooftop solar data in 2024, rooftop capacity connected to the grid has increased by 30MW a year, in line with the government’s stated quota.

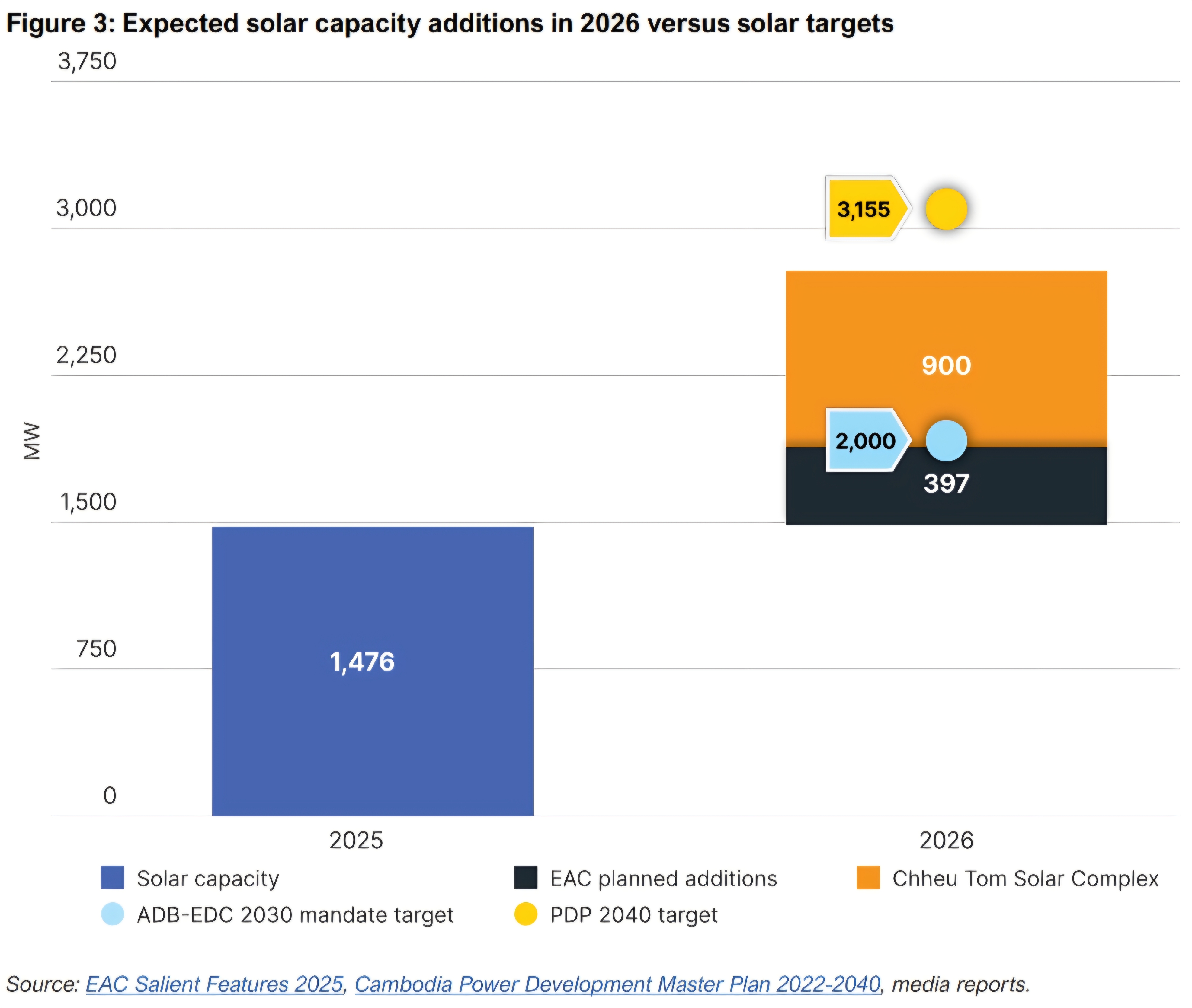

The completion of several solar power projects in 2026 should increase capacity by almost 400MW, bringing it to approximately 1.87GW by year-end. The EAC projects that solar will supply more than 12% of Cambodia’s electricity requirements.

The commissioning of Southeast Asia’s largest solar facility — the Chheu Tom Solar Complex — in March 2026 could boost capacity by another 930MW. This alone would push capacity above the 2GW target set in a 2022 mandate between the Asian Development Bank (ADB) and the state-owned Electricite du Cambodge (EDC).

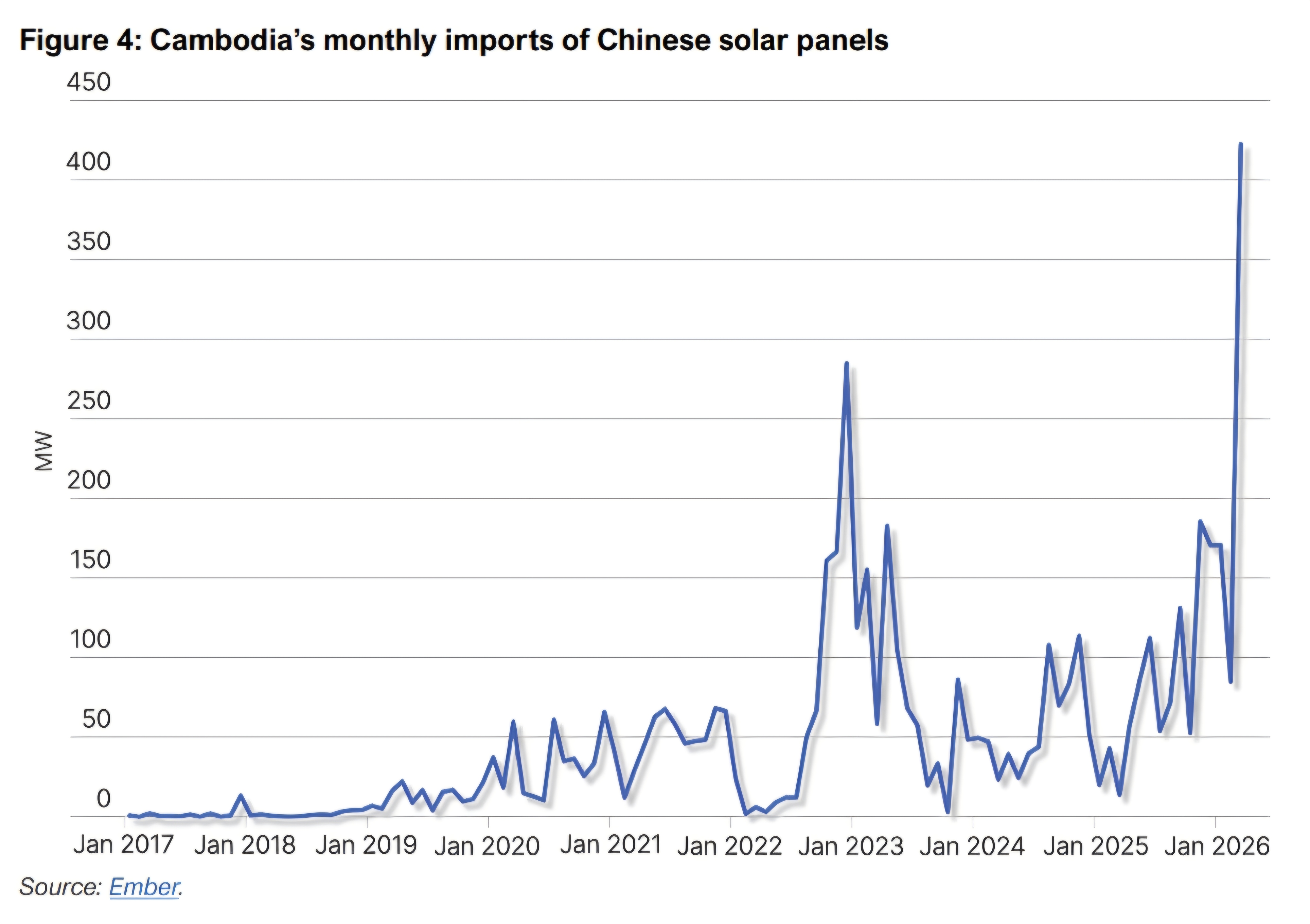

Furthermore, Cambodia’s imports of solar panels from China suggest that capacity additions could increase further, putting the 2040 PDP targets within reach. According to data from Ember, the bulk of Cambodia’s 1GW of solar panel imports from China in 2025 occurred in the second half of the year. Since it takes months to commission panels, many of these imports have yet to be installed and are not producing power.

The current Middle East conflict could also prompt consumers to reduce their exposure to surging, volatile fossil fuel prices by adopting solar and other low-emitting technologies.

Monthly Chinese solar panel import data from Ember suggest that such a response may already be occurring. In March 2026 — the first month after the conflict started — solar panel imports jumped to an all-time monthly high of 422MW. This exceeds EAC’s expected capacity increase of 397MW for grid-connected solar in 2026.

Policy responses to the crisis are also likely to incentivize further imports. Effective 1 April 2026, the Cambodian government reduced import taxes on several technologies — including solar power and energy storage systems such as batteries — from 15% to 0%. This cost reduction could accelerate the import and deployment of utility-scale solar. One solar manufacturer estimates that this tax reduction could lower installation costs by up to 30%. Even under more conservative assumptions, the Institute for Energy Economics and Financial Analysis (IEEFA) estimates that total costs could be reduced by approximately 7.4%.

Cambodia has substantial potential to expand its solar capacity. In 2016, the ADB estimated Cambodia’s solar potential at 8.1GW, while in 2021, a technical assessment found a 44GW possibility. Moreover, the ADB is helping fund grid upgrades to integrate surging solar and wind power into the generation mix.

Barriers to adopting rooftop solar

Despite recent progress, persistent policy barriers could continue to constrain rooftop solar deployment in Cambodia.

Cambodia has some of the highest electricity tariffs in Southeast Asia. Consequently, rooftop solar presents a significant opportunity for consumers and the EDC to reduce electricity expenditure. Even with an estimated levelized cost of electricity (LCOE) of USD0.135 per kilowatt-hour (kWh) in 2019, captive rooftop solar could compete with the high tariffs paid by commercial and industrial users.

However, government concerns about grid reliability and the cost impacts of rooftop solar have led to the introduction of several barriers to adoption. The most significant was a capacity charge established in 2018 that raised rooftop solar costs well above the EDC tariff. Other barriers include restrictions on time-of-use pricing for solar systems, a limit on solar system sizes to 50% of the contracted load, and a prohibition on exporting excess solar generation to the grid.

Beginning in 2023, the government began replacing the capacity charge mechanism with a compensation tariff system and easing some restrictions. For example, the system capacity limit was removed, and rooftop solar users were permitted to export excess solar to the EDC grid, albeit without financial compensation.

Nevertheless, the replacement compensation tariff continues to present challenges similar to those associated with the previous capacity charge mechanism.

Compensation tariff

Following several years of stakeholder consultations, the solar compensation tariff scheme was enacted in June 2025. The MME designed the tariff to ensure that solar adopters contributed to the costs associated with using the national grid and maintaining generation capacity requirements.

A compensation tariff that undermines rooftop solar adoption

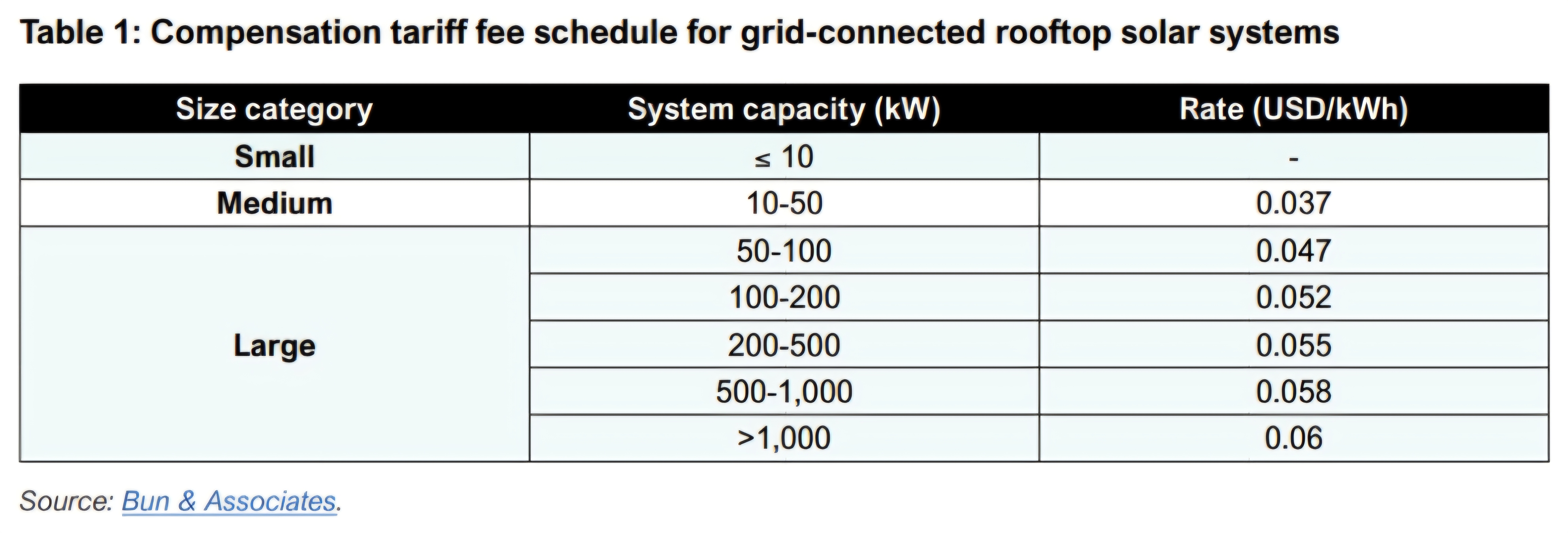

The MME outlined that the EAC would calculate the compensation tariff based on the difference between the general electricity tariff and the cost of solar generation for small, medium, and large customers. Calculated this way, the compensation tariff would effectively eliminate the financial incentive to install rooftop solar systems. The EAC reviews these tariffs at least once a year to ensure that they continue to align with these principles.

Commercial and industrial stakeholders engaged with the government for nearly two years during the development of the compensation tariff schedule. Stakeholders broadly agreed with the principle of setting a compensation tariff “to reflect the cost of maintaining the grid and integration of renewable energy sources”. The European Chamber of Commerce in Cambodia (EUROCHAM) and the Textile, Apparel, Footwear and Travel Goods Association in Cambodia (TAFTAC) highlighted that a compensation tariff starting at USD0.01/kWh for medium systems and increasing to USD0.02/kWh for large systems would adequately compensate the EDC. However, the final compensation tariff schedule was set at rates three to four times higher than those proposed by industry stakeholders. EUROCHAM and TAFTAC warned that these tariffs would halt installations of solar rooftop systems in commercial, industrial, and large residential applications. EAC data reveals that as of 2025, only 0.02% of Cambodia’s grid connections have installed a registered solar photovoltaic (PV) system.

The compensation tariff applies to all power generated from grid-connected solar systems larger than 10 kilowatts (kW), starting at USD0.037/kWh and scaling up to USD0.06/kWh for systems exceeding 1MW. Solar installations in off-grid areas are not required to pay the tariff.

With the final compensation tariff higher than the capacity payment it replaced, stakeholders questioned whether the tariff design excessively compensates for grid impact, potentially shielding the state-owned utility from solar competition.

IEEFA’s analysis of the impact of the compensation tariff on solar adoption costs suggests that the fees are structured more to protect the national utility than to recover actual grid integration costs.

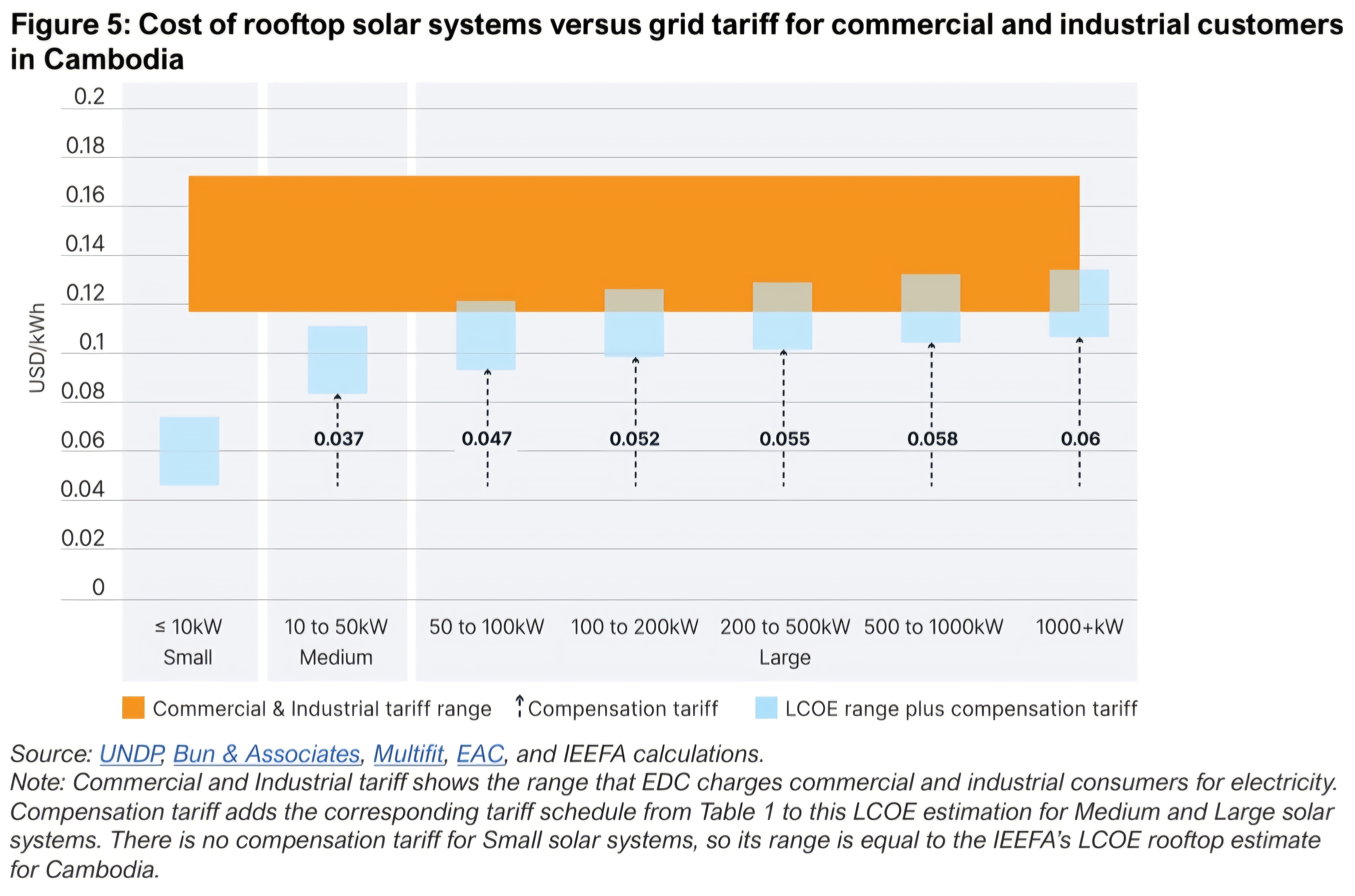

Accounting for the recent elimination of import duties and current system prices, IEEFA estimates that the LCOE of rooftop solar in Cambodia ranges from USD0.046/kWh to USD0.074/kWh. For a residential installation of 10kW — exempt from the compensation tariff — solar is competitive with EDC residential rates, which range from USD0.095/kWh to USD0.182/kWh.

However, the progressive structure of the compensation tariff schedule erodes the financial benefits of installing medium and large solar systems (Figure 5). IEEFA estimates that the compensation tariff extends the payback period for rooftop solar installations by nearly two years, in line with assessments by EUROCHAM and TAFTAC. Moreover, with the EDC electricity tariff ranging between USD0.117/kWh and USD0.172/kWh for commercial and industrial activities, the compensation fee tariff could eliminate savings from both medium and large solar system installations for some consumers.

Compensation tariff complexity for BESS-equipped systems discourages adoption

For systems equipped with a battery energy storage system (BESS), the compensation fees are conditional on the level of battery discharge. If monthly BESS discharge equals or exceeds 50% of the solar system’s production in a month, the adopter is exempt from paying compensation. If the discharge level is under 50%, the monthly compensation fee is calculated by subtracting double the battery discharge from the energy generated from the rooftop system, multiplied by the corresponding compensation tariff rate:

Compensation Fee = {Energy generated by the rooftop solar system (RTS) (kWh) - [2 × Energy from BESS (kWh)]} × Compensation tariff rate (USD/kWh from Table 1)

Due to the fluctuating profile of solar generation, this formula introduces uncertainty into the operating costs of rooftop solar adoption.

Frequent and open-ended compensation review process deters solar deployment

The frequent compensation tariff review process adds further uncertainty for potential adopters. The EAC is tasked with reviewing the compensation tariff every six to twelve months to ensure it reflects the difference between the general retail rate and the cost of solar generation. Consequently, potential adopters cannot reliably forecast the tariff beyond the near term, adding uncertainty to the rooftop solar adoption process.

Grid-connected solar quota

Another barrier to solar adoption is the rooftop solar quota. Since 2025, the MME has set an annual limit of 30MW for grid-connected rooftop solar installations. Together with the EDC, the MME distributes this quota across the country’s provinces and zones. If the EAC determines that an application for rooftop solar will exceed any of these quotas, the application is rejected. Some experts suggest that if registrations exceed the quota early, there could be pressure to lift it in 2026 and subsequent years.

Currently, however, the 30MW annual quota could constrain the adoption of solar outside the utility-scale model prioritized by the government.

Rooftop solar barriers undermine industrial competitiveness

These rooftop solar barriers are a competitive issue for Cambodia’s industrial sector.

In a 2022 position paper, a coalition of garment and apparel manufacturers argued that a supportive rooftop solar framework was essential to strengthening the competitiveness and long-term prospects of the Cambodian industry and the broader manufacturing sector. Expanding rooftop solar installations would lower energy costs by reducing consumption of expensive grid electricity, unlock carbon-conscious export markets, and attract new investments from suppliers committed to decarbonizing their supply chains.

While capacity payments have been successfully removed, the replacement compensation tariff continues to deter solar deployment for commercial and industrial adopters. TAFTAC identifies high electricity prices and the compensation tariff as weaknesses of locating Garment, Footwear, and Travel Goods (GFT) production in Cambodia. Given that GFT accounts for about half of all exports, rooftop solar barriers pose a risk to the country’s economic development and industrial competitiveness.

The entrance of LNG-to-power

The operation of Cambodia’s first high-cost, large-scale LNG-fired plant could add to the urgent need to address barriers to solar adoption.

The 900MW power plant and import terminal, developed by the Royal Group, is expected to deliver power in two 450MW phases, the first by the end of 2026, and the second in 2027.

While the government views the project as supporting long-term energy resilience, introducing LNG into the energy system could negatively impact industrial competitiveness by reducing reliability and raising electricity prices.

High-cost LNG will likely inflate Cambodia’s already-high electricity costs

Once fully operational, the Royal Group project is expected to generate approximately 6,000 gigawatt-hours (GWh) of electricity annually, supplying around 23% of the country’s electricity needs and requiring an estimated 0.75 million tonnes of LNG imports per year.

Over the past decade, Cambodia lowered its electricity tariffs by integrating large-scale, low-cost power projects to replace high-cost, smaller-scale oil-fired projects. Tying almost a quarter of electricity supply to a 30-year take-or-pay LNG contract risks reversing these gains.

Given the project’s higher generation costs, large scale, and long-term take-or-pay power purchase agreement (PPA), Cambodia’s first LNG-to-power project is likely to exert upward pressure on retail tariffs when it starts operating.

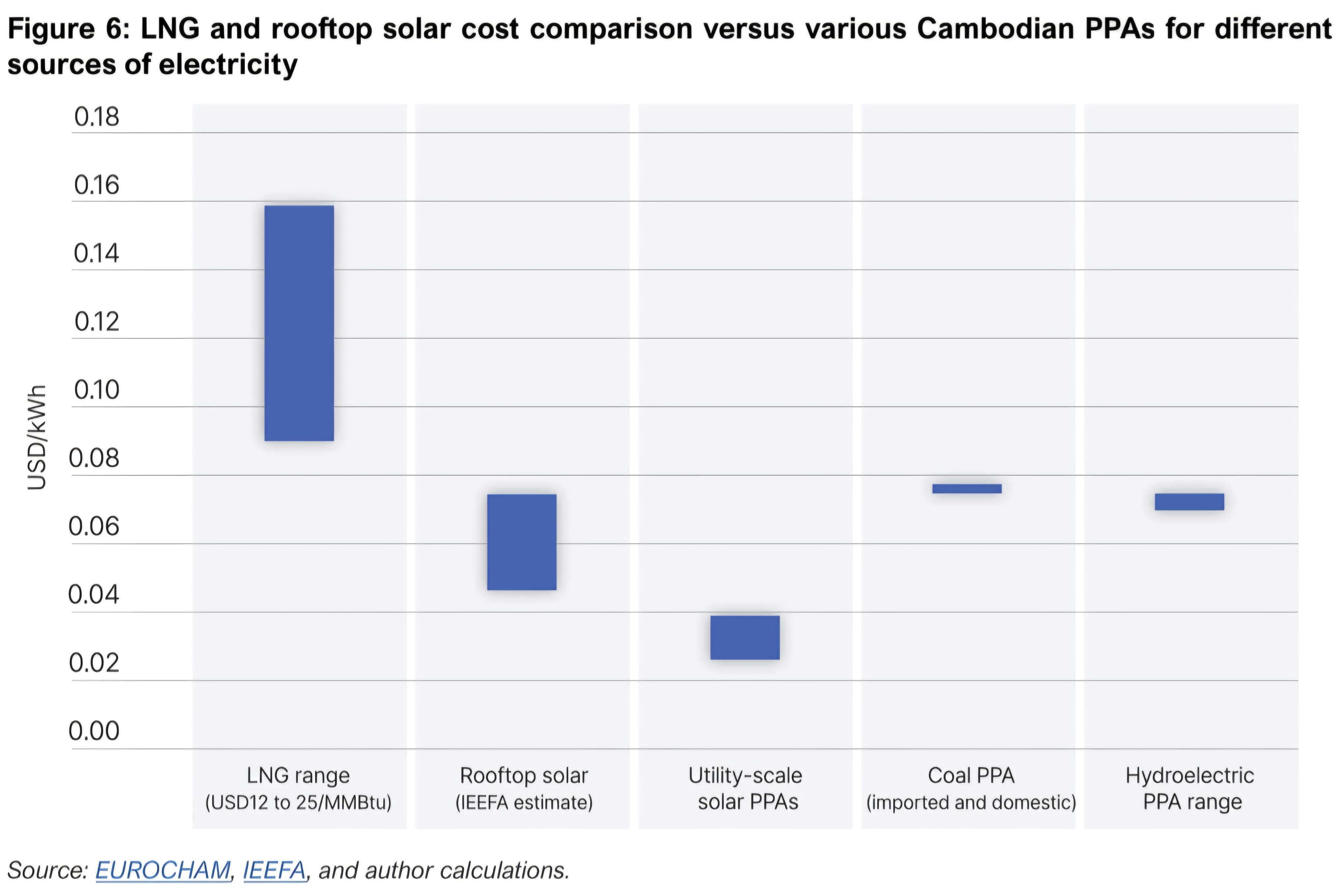

IEEFA estimates that the Royal Group project will generate electricity at an average cost of around USD0.12/kWh, based on recent LNG prices of USD17 per million British thermal units (MMBtu). Costs could rise to USD0.16/kWh if LNG prices increase to USD25/MMBtu. Alternatively, costs could fall to USD0.09/kWh if Cambodia secures LNG at USD12/MMBtu. However, as a relatively new LNG importer with lower demand volumes than established buyers, Cambodia is likely to have limited bargaining power to negotiate favorable pricing for cargo deliveries. Several smaller LNG importers, including Myanmar, the Philippines, and Vietnam, remain heavily reliant on volatile spot markets to meet their requirements.

Meanwhile, the ongoing Middle East conflict and the Strait of Hormuz closure could exert lasting upward pressure on prices over the next few years. Restarting production from Qatar cannot begin until hostilities ease. Repairing damage to QatarEnergy’s LNG-producing facilities — which account for about 3% of global supply — could take up to five years and delay ongoing expansions.

Therefore, producing LNG-fired power at a cost under USD0.12/kWh appears unlikely.

The estimated generation costs of the 900MW LNG-to-power project surpasses several known electricity contract prices currently paid by EDC and are also higher than IEEFA’s estimated rooftop solar costs.

With transmission and distribution charges likely to add USD0.10/kWh to the retail tariff, the cost of LNG-fired electricity delivered to consumers could range from USD0.19/kWh to USD0.25/kWh. This is well above the current tariffs paid by consumers, with industrial rates peaking at USD0.150/kWh, commercial rates at USD0.177/kWh, and the highest residential rates at USD0.18/kWh. Unless industrial consumers near the Royal Group facility commit to purchasing LNG-fired electricity directly, consumer rates across Cambodia will need to rise to cover the higher cost of this electricity.

Economic crises can further challenge LNG’s affordability and reliability

While proponents champion LNG-to-power projects as a balanced solution for reliability and affordability, experience across Asia suggests otherwise.

In practice, LNG-to-power projects often create reliability challenges, especially for smaller importers during crises. This largely stems from the high, recurring fuel costs of purchasing LNG cargoes that are denominated in US dollars and subject to global market volatility.

LNG cargo costs can be compounded by currency devaluation, which often occurs during commodity crises, straining currency reserves. This can prompt LNG suppliers to demand premiums, further inflating already high costs. When debt repayments are delayed to prioritize higher fuel costs, external refinancing may follow, often with austerity covenants that eliminate subsidies protecting households and strategic industries. For smaller importers like Cambodia, competing with wealthier buyers for finite cargoes in a tight market poses affordability and energy security risks.

Bangladesh case study

Bangladesh’s experience is particularly instructive for Cambodia, which relies on the apparel sector for the bulk of its export earnings.

Bangladesh’s rising dependence on LNG imports increased subsidies and eroded currency reserves during the last energy crisis. Loans secured to refinance unpaid fossil fuel import debts came with conditions requiring the phaseout of subsidies, eventually aligning energy prices with procurement costs. Meanwhile, disruptions at floating import terminals — some lasting up to six months — led to significant outages and blackouts.

This has been significantly detrimental to the competitiveness of garment manufacturers in Bangladesh — the world’s second-largest ready-made garment (RMG) exporter. Energy costs doubled, undermining industrial competitiveness, while gas disruptions caused widespread curtailment and factory shutdowns. Unable to fulfill contracted deliveries, manufacturers lost orders as foreign buyers turned to other countries.

Meanwhile, apparel supply chain investors are increasingly factoring power supply reliability into sourcing and manufacturing decisions. With insights from Bangladesh’s experience in mind, Cambodia’s future competitiveness will depend on mitigating the reliability and affordability challenges posed by LNG.

Embracing rooftop solar could help ease the LNG burden

Cambodia’s rapid adoption of utility-scale solar has elevated the country to a renewable energy leader among its peers in the Association of Southeast Asian Nations (ASEAN).

While this progress has helped insulate Cambodia from the economic impacts of the Middle East conflict, the introduction of LNG risks drawing the country into the enduring regional energy crisis.

By matching its prioritization for utility-scale solar with a similar adoption of rooftop solar, Cambodia could further shield consumers and the EDC from the inflationary impact of LNG imports.

The EDC currently absorbs excess rooftop solar capacity from the grid at no cost, but the compensation tariff is constraining rooftop adoption among industry, businesses, and households. Given strong interest from Cambodia’s key manufacturing stakeholders, replacing this tariff with a more supportive compensation regime would likely accelerate adoption.

While adopters would prefer a net-metering scheme, the current compensation tariff penalizes rooftop solar to such a high degree that even modest reform would incentivize installations. As outlined by EUROCHAM and TAFTAC, a reduction between USD0.01/kWh and USD0.02/kWh would be acceptable to garment and other manufacturers.

The EDC could also benefit from expanded rooftop solar deployment. With electricity costs set to rise as the 900MW Royal Group facility becomes operational, the state-owned utility could offset the high cost of LNG-fired electricity with low-cost solar, limiting the financial impact on ratepayers.

Multilateral finance could help address the EDC’s concerns over the grid impacts of a potential rooftop solar boom. Development banks have been integral to unlocking record-low solar auctions and financing grid upgrades to absorb new renewable capacity in some of the world’s fastest-growing electricity markets. Similar financing packages for grid upgrades to integrate distributed resources from prosumers could help alleviate the costs of rooftop solar integration.

Accelerating the deployment of batteries, such as the recently commissioned 0.5GW/1GWh BESS facility in the Pursat province, could also support the grid and integrate additional solar resources. According to the International Renewable Energy Agency (IRENA), pairing solar with BESS is now competitive with most fossil fuel generation, including LNG-fired power plants, in high-quality solar regions.

Conclusion

Despite significant barriers to rooftop solar, Cambodia ranks among regional leaders in the solar share of its generation mix. Ahead of hosting the 3rd International Conference on Fossil Fuel Phase-Out, the country has a clear opportunity to cement its status as a global leader in renewable energy.

Removing the remaining rooftop solar barriers will strengthen the competitiveness of its manufacturing base, build economic resiliency, and position Cambodia as a prominent participant in the global energy transition — reducing its exposure to future fossil fuel disruptions.

Related Content