Key Findings

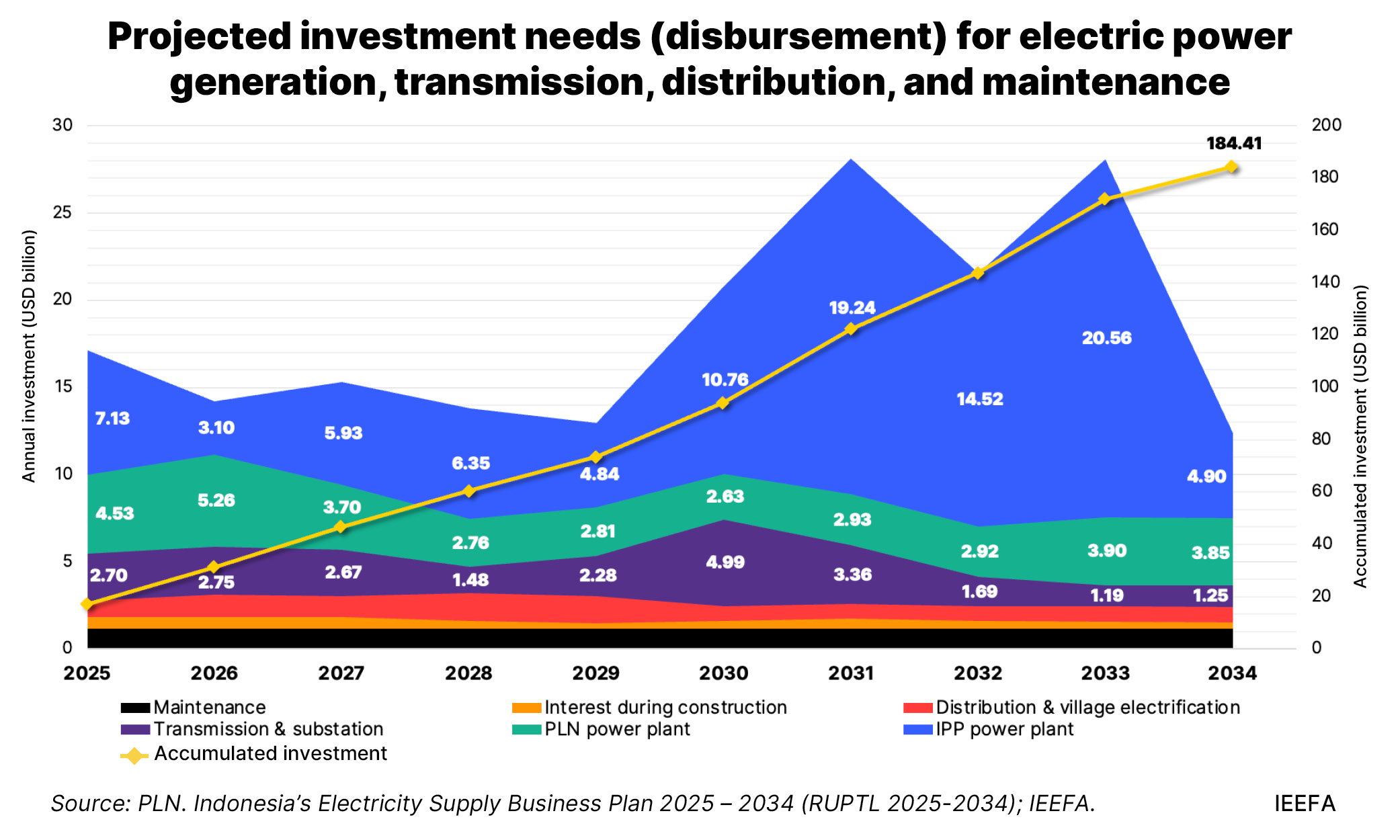

Indonesia's Electricity Supply Business Plan (RUPTL) 2025–2034 requires an average annual transmission investment of USD2.4 billion to support large-scale renewable energy deployment, industrial electrification, and inter-island grid integration. Realized investment has averaged only USD1.4 billion annually since 2019. Closing this gap requires structural reform to transmission financing, not just increased budget allocations.

Indonesia’s electricity transmission is financed through the national electricity utility PLN’s consolidated balance sheet, blending its low-risk profile with fuel price volatility, foreign exchange exposure, and subsidy risk. This misalignment inflates financing costs, obscures grid expenses, and risks turning transmission into a bottleneck for the energy transition.

Establishing a separate PLN transmission company through corporate restructuring and financial ring-fencing within a state-owned framework offers a pragmatic solution. Clearly defining transmission assets, costs, and revenues would allow regulated tariffs to support cost recovery, unlock long-term infrastructure finance, and reduce reliance on national budgets while preserving state control.

Transmission separation experience from India and Vietnam demonstrates that comparable ring-fencing within PLN could unlock lower-cost, long-term transmission financing, and improve investment scale and transparency. It would also support renewable energy integration and regional electricity exports, and strengthen financial sustainability, without altering state ownership or Indonesia’s constitutional framework.

Executive Summary

Indonesia is a growing economy — driven by rapid electrification, rising industrial demand, ambitious renewable energy targets, and emerging export opportunities — that requires sustained, long-term grid investment. However, delays in expanding and modernizing the country’s electricity transmission network are constraining economic growth, renewable energy deployment, and regional electricity trade. Current institutional and financing frameworks are not designed to deliver investment at the required scale or pace.

Transmission is a capital-intensive, long-term infrastructure asset with stable and predictable usage patterns. When financed as a low-risk regulated utility, it can attract long-tenor capital at interest rate spreads close to those of sovereign borrowing. However, within Indonesia’s national electricity utility, PT Perusahaan Listrik Negara (PLN), transmission investment competes with generation and supply activities that carry different risks and policy obligations, including fuel price volatility, foreign exchange exposure, subsidy timing risk, and long-term power purchase commitments. As a result, the inherently lower-risk profile of transmission is embedded within PLN’s broader capital structure and priced according to the utility’s blended corporate risk rather than its stand-alone level. This misalignment increases financing costs, obscures the true economics of grid infrastructure, and risks turning transmission into a bottleneck in Indonesia’s energy transition.

Establishing a separate PLN transmission company through corporate restructuring and financial ring-fencing within a wholly or majority state-owned framework offers a practical solution. By clearly defining transmission assets, costs, and revenues, regulated tariffs could support cost recovery and facilitate access to long-term infrastructure finance, reducing reliance on state budgets while preserving state control.

Transmission separation would not imply privatization, market liberalization, or constitutional unbundling. Transmission would remain a regulated monopoly under state ownership and government oversight, consistent with Indonesia’s Electricity Law and recent Constitutional Court rulings. Rather, the reform would be institutional and financial in nature, aimed at improving transparency, accountability, and investment capability to raise capital for Indonesia’s ambitious transmission expansion and modernization plans.

This report provides case studies of alternative corporate structures that have enabled similar entities in India and Vietnam to consistently raise substantial capital. Power Grid Corporation of India Limited (PGCIL) is a majority government-owned, corporatized, and commercially-oriented pure transmission entity that operates under an independent, rate-of-return regulatory structure. The company has domestic and foreign bond ratings that underpin a robust debt issuance program. Corporate financial credibility is further supported by listings on domestic stock exchanges, requiring transparent accounting and financial reporting in accordance with regulatory obligations for listed entities. PGCIL has eliminated the need for public budget allocations, and sovereign guarantee support is limited to legacy multilateral development bank debt on its balance sheet. This approach allows PGCIL to self-finance an average of USD2.5 billion in capital investment in grid development each year over the past decade1 — an amount similar to what PLN requires for its investment plans.

State-owned power company Electricity of Vietnam (EVN) operates under a universal service mandate and a base tariff structure similar to PLN. EVN has established wholly-owned subsidiaries for generation, distribution, and transmission. The transmission entity, National Power Transmission Corporation (EVNNPT), was created to rationalize system expansion and operations. EVN is actively structuring and positioning EVNNPT’s corporate operations to support an international credit rating and broaden access to capital from diverse sources.

Clear governance also allows these separate transmission utilities to deliver on investments that create broader benefits for their national energy sector and economy. For Indonesia, a dedicated PLN transmission subholding would support large-scale renewable integration, enable electricity export projects to be financed on cost-reflective transmission tariffs, and strengthen the country’s position in regional initiatives such as the Association of Southeast Asian Nations (ASEAN) Power Grid. International experience demonstrates that regulated, state-owned transmission infrastructure can be both financeable and commercially viable.

The establishment of Danantara, Indonesia’s sovereign wealth fund tasked with holding and managing the country’s state-owned enterprises — including PLN — further sharpens the case for reform. Danantara's mandate is to allocate state capital on a disciplined, returns-based foundation. This directive is challenging given the current transmission structure, where investment is recorded as an undifferentiated line item on PLN's consolidated balance sheet. A ring-fenced transmission company would create the institutional platform necessary for Danantara, alongside other domestic and international institutional financiers, to invest in grid expansion on terms that reflect transmission's stand-alone risk profile.

This report finds that transmission separation is not an end in itself, but an enabler of national electricity system improvement and cost-effectiveness. Aligning grid governance and financing efficiency with the underlying economics of transmission infrastructure can reduce system costs, accelerate renewable energy deployment, and support Indonesia’s long-term economic and energy objectives. With national plans for grid expansion exceeding USD24.4 billion over the next 10 years and complementary renewable energy additions four times that amount, the energy transition cannot be funded solely by the state budget. The framework proposed in this analysis is designed to build the institutional and financial capacity for PLN's transmission function to progressively self-fund its expansion, alongside support from the state, Danantara, and capital markets.

1 Power Grid Corporation of India Ltd. Annual Reports, FY 2016-2017 to FY 2024-2025.

Related Content